[ad_1]

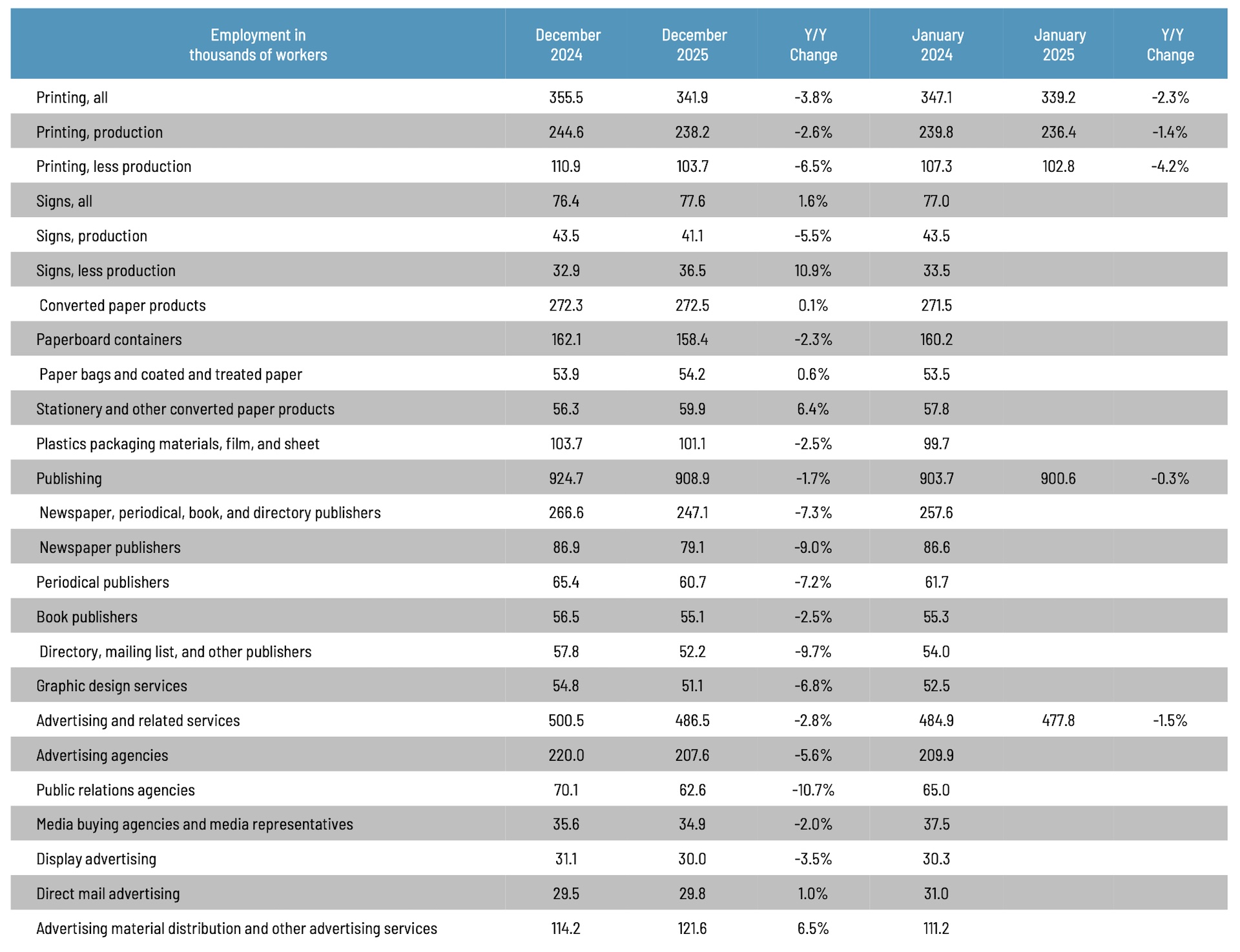

When last we checked in with printing employment, it had been generally flat throughout the summer and fall. We missed a month due to the government shutdown, and maybe we should shut down again because we kicked off the year with a 2.7% decrease in overall industry employment, with production employment down 1.8% and non-production employment down by 0.9%.

Publishing employment was down 0.9% from December to January.

Looking at other business categories, the reporting of which lags a month:

Overall employment in the signage industry was up 2.9% from November to December 2025, with sign production employment up 3.3%, and non-production up 2.5%.

On the other hand, converted paper products employment was down 0.8% from November to December, with paperboard container employment down 2.0% and paper bags and coated and treated paper employment down 0.9%.

Looking at some specific publishing and creative segments, from November to December, periodical publishing employment was down—yikes—3.5%, newspaper publishing employment was down 1.9%, and book publishing was down 2.5%. Graphic design employment was down 2.7%, ad agency employment was—double yikes—down 4.9%, and PR agency employment was down 4.1%. Weirdly, direct mail advertising employment won the month, employment being up 6.0% from November to December. Go figure.

As for January employment in general, it was strong in some ways, weak in others. The BLS reported on February 11:

Total nonfarm payroll employment rose by 130,000 in January, and the unemployment rate changed little at 4.3 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, social assistance, and construction, while federal government and financial activities lost jobs.

The U-6 rate (the so-called “real” unemployment rate which includes not just those currently unemployed but also those who are underemployed, marginally attached to the workforce, and have given up looking for work) decreased from 8.4% to 8.0%.

The labor force participation rate increased in September from 62.4% in December to 62.5% in January and the employment-to-population increased from 59.7% to 59.8%. The labor force participation rate for 24–54-year-olds increased from 83.8% to 84.1%.

The January numbers were better than what economists had expected. That was the good news. The bad news is:

The change in total nonfarm payroll employment for November was revised down by 15,000, from +56,000 to +41,000, and the change for December was revised down by 2,000, from +50,000 to +48,000. With these revisions, employment in November and December combined is 17,000 lower than previously reported.

But the really bad news was the annual revision to overall 2025 employment.

The seasonally adjusted total nonfarm employment level for March 2025 was revised downward by 898,000. On a not seasonally adjusted basis, the total nonfarm employment level for March 2025 was revised downward by 862,000, or -0.5 percent. Not seasonally adjusted, the absolute average benchmark revision over the prior 10 years is 0.2 percent.

The change in total nonfarm employment for 2025 was revised from +584,000 to +181,000 (seasonally adjusted).

Yikes. That works out to an average of only 15,000 jobs added per month in 2025. Let’s hope January’s numbers are a positive omen for 2026—although our own industry employment situation is worrisome.

[ad_2]

Source link